CCLP’s newest report series focuses on economic policy and young adulthood in Colorado and the ways in which public benefits do and do not support their needs.

Recent articles

CCLP comments on Xcel Energy’s proposed rate increase

Milena Tayah provided comments to the Public Utilities Commission regarding Xcel Energy’s proposed rate increase on Colorado consumers’ energy bills.

2026 Legislative wrap-up, part 2

Part 2 of CCLP’s 2026 legislative wrap-up, including defending public programs, strengthening consumer rights, and looking to the future.

2026 Legislative wrap-up, part 1

Part 1 of CCLP's 2026 legislative wrap-up, including advocacy work, policy priorities, and advancing economic justice.

Scorecard reveals challenges for Colorado families

Seven years since the official end of the Great Recession, many economists agree that America’s agonizingly slow financial recovery is finally complete. But even though the national unemployment rate has remained steady in recent months, it’s clear to many families that the widespread economic prosperity of the past is just that—a thing of the past.

Recently, CCLP’s partners, CFED (the Corporation for Enterprise Development) released the 2016 Assets & Opportunity Scorecard. The report evaluates 69 different policy measures to determine how well states are addressing the challenges facing their residents. In short, the scorecard illustrates that financial vulnerability is the norm in Colorado and nationwide. And for those who were just scraping by before the recession, the struggles have only deepened.

The situation is especially dire for households of color, which are more than twice as likely as white households to live below the federal poverty level and 1.7 times more likely to lack liquid savings.

Why are so many households living in such a financially precarious position? Findings from the Scorecard reveal some answers:

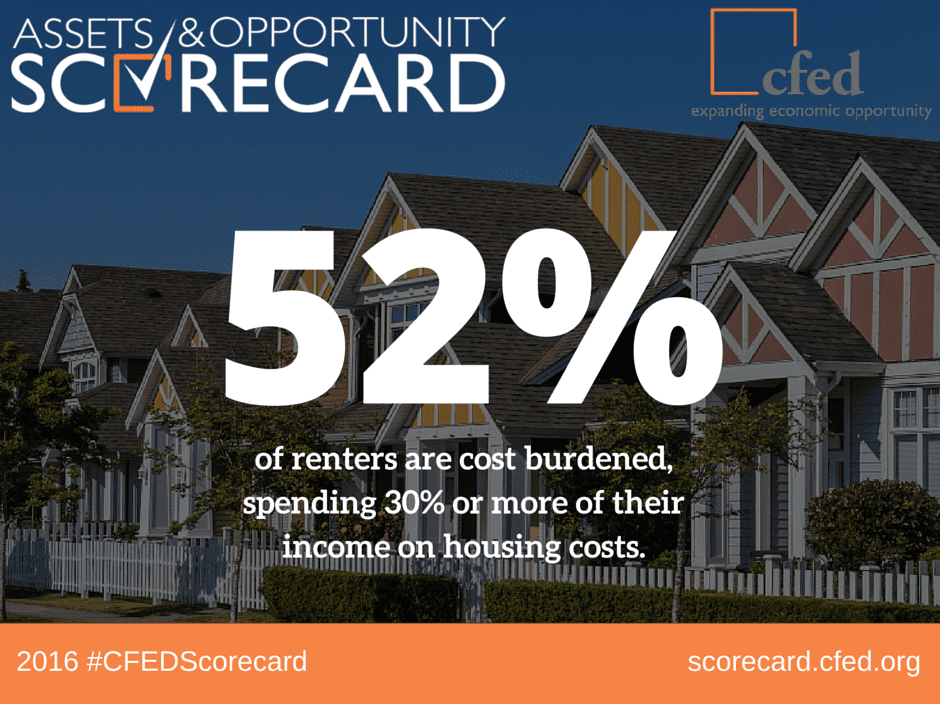

- There is a significant affordable rental housing shortage nationally and in many states. As a result, more than half (51.8 percent) of renters are cost-burdened, which means they spend more than 30 percent of their income on housing. Colorado is consistent with the national norm with 52 percent of cost-burdened renters spending more than 30 percent of their income on housing.

- Outsized spending on housing reduces funds for food, health care, child care and other basic needs. Typically, health care is the first to go; 14.3 percent of adults say they didn’t see a doctor over the last year because of cost. The statistics are worse for adults of color; one in four Latino adults and one in five African-American adults said financial concerns prevented them from seeing a doctor.

- The scorecard shows that 39 percent of Colorado’s households are locked into a “new normal” of perpetual financial insecurity, unable to build the savings needed to last even three months in the event of an emergency.

- Colorado’s 9th-place outcome ranking improved from last year’s 13th-place ranking. The state received an “A” in Education, driven in part by having the third-highest rate of degree attainment from two- and four-year colleges (46.6 percent and 38.3 percent, respectively). Colorado’s low underemployment rate (8.4 percent) relative to the national average (10.8 percent) helped the state also earn an “A” in Businesses & Jobs. The state’s worst grade was a “C” in Health Care, due partially to its high rate of uninsured low-income children (8.1 percent), and disparities in insurance by race and gender. Coloradans of color are 2.3 times more likely to be uninsured than white Coloradans, and women in the state are 1.3 times more likely to be uninsured than their male counterparts. The state received a “B” in both Financial Assets & Income and Housing & Homeownership.

- Nationwide, households just aren’t bringing in enough income to cover basic expenses. One in four jobs in the US today is in a low-wage occupation, and the underemployment rate—the number of unemployed, plus those who have part-time work but seek full-time employment, along with those who have given up because they are discouraged by the job market—is still double that of the unemployment rate, at 10.8 percent.

- Even people of color who started their own businesses to make it through the Great Recession are falling farther behind. While the latest data show that the average value of minority-owned businesses increased by nearly $22,000 (10.8 percent) since 2007, the average white-owned businesses saw their value rise by more than $121,000 (22.6 percent) during that same period. The average white-owned business now is worth $656,364, compared to just $224,530 for a minority-owned business.

As grim as these numbers are, there are numerous tested solutions that can be leveraged to help build an opportunity economy in which everyone has the chance to succeed. Take the Earned Income Tax Credit (EITC)—the most effective anti-poverty program in the country. The EITC increases the incomes of hard-working families struggling to cover basic expenses and enables families to start saving for a more secure financial future—and policymakers on both sides of the aisle agree that it works. It is time to expand policies—at the federal, state and local levels—that work to increase financial security and reduce inequality. In Colorado, CCLP was part of a coalition, led by the Colorado Fiscal Institute, which successfully advocated for activating the EITC statewide in 2015.

To learn more about policies that help to build an opportunity economy, and for a full analysis state- and national-level outcome and policy data across 130 different measures, visit http://scorecard.cfed.org.

For a rundown of statewide results, visit the Colorado state profile on CCLP’s website. CCLP partners with CFED as the state leader of its Assets & Opportunity Network.

– CFED

Recent articles

Economic policy and young adulthood in Colorado: A new report series from CCLP

CCLP’s newest report series focuses on economic policy and young adulthood in Colorado and the ways in which public benefits do and do not support their needs.

CCLP comments on Xcel Energy’s proposed rate increase

Milena Tayah provided comments to the Public Utilities Commission regarding Xcel Energy’s proposed rate increase on Colorado consumers’ energy bills.

2026 Legislative wrap-up, part 2

Part 2 of CCLP’s 2026 legislative wrap-up, including defending public programs, strengthening consumer rights, and looking to the future.

2026 Legislative wrap-up, part 1

Part 1 of CCLP's 2026 legislative wrap-up, including advocacy work, policy priorities, and advancing economic justice.